What Happened: Visa launched Intelligent Commerce Connect on April 8, 2026, a platform that lets AI agents initiate purchases, handle tokenization, enforce spend controls, and authenticate payments on behalf of users. It supports four major agent protocols and is currently in pilot with partners including AWS and Highnote. This is the first major payment network to formally open its infrastructure to agentic commerce.

AI shopping agents have had a credibility problem for years. They could browse, add to cart, and find the best deal. They could not pay without handing control back to a human.

Visa just fixed that.

Visa’s Intelligent Commerce Connect, announced April 8, 2026, gives AI agents a formal path to completing purchases end-to-end, with tokenization, spend controls, and fraud authentication built in.

This isn’t a theoretical roadmap. It’s in pilot with real partners right now.

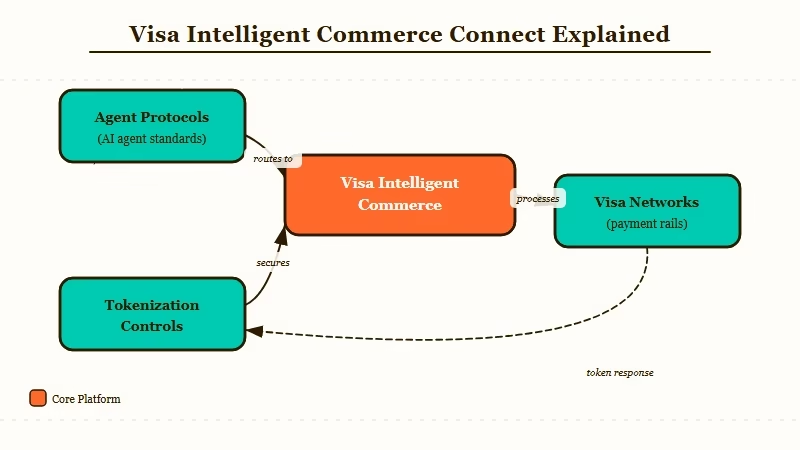

What Is Visa’s Intelligent Commerce Connect?

Visa’s Intelligent Commerce Connect is a single integration point that lets AI agents initiate and complete payments, covering tokenization, spend controls, and authentication across Visa and non-Visa networks.

The platform connects to Visa through the Visa Acceptance Platform and functions as a protocol-agnostic layer, meaning it doesn’t lock agents into one specific agentic framework.

From what I’ve seen with payment infrastructure plays, that multi-protocol approach is the smart move. Visa has explicitly built in support for four agent protocols:

- Trusted Agent Protocol (TAP): the authentication handshake between user and agent

- Machine Payments Protocol (MPP): handles machine-to-machine payment instructions

- Agentic Commerce Protocol (ACP): governs how agents discover and select products

- Universal Commerce Protocol (UCP): the broader interoperability layer across platforms

Merchants who integrate get a second benefit: their product inventories and details become discoverable to AI agents directly, meaning a shopping agent can search a merchant’s catalog without ever opening a browser window.

| Capability | What it covers |

|---|---|

| Payment initiation | Agent triggers purchase without human input |

| Tokenization | Card details are never exposed to the agent directly |

| Spend controls | Users set per-agent or per-session spending limits |

| Authentication | Fraud detection runs on the Visa network, not the agent |

| Network support | Works with Visa and non-Visa cards |

| Inventory access | Merchants expose their catalog to agentic discovery |

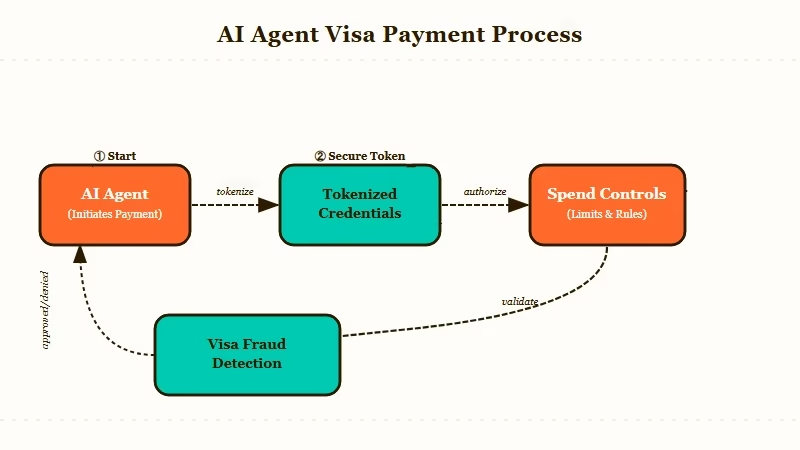

How Do AI Agents Pay for Things Through Visa?

AI agents pay through Visa’s Intelligent Commerce Connect by receiving a tokenized credential from the user’s account, which the agent uses to initiate payment without ever accessing raw card data.

The way I’d explain the trust model here is: the card never touches the agent. Visa issues a token for a specific agent, tied to spend controls set by the user. The agent uses that token to pay.

If the agent goes rogue or gets compromised, the token can be revoked without affecting the underlying card account. This is the piece that was missing from every “AI shopping agent” demo before this.

Without a secure tokenization layer, any agent capable of paying was also capable of leaking your payment credentials or making unapproved purchases.

With Visa’s infrastructure in the middle, those risks shift to Visa’s existing fraud detection apparatus.

Current pilot partners include Aldar, AWS, Diddo, Highnote, Mesh, Payabli, and Sumvin. Visa has said the rollout extends to more partners through 2026.

What Does This Mean for AI Tool Users?

For people using AI tools right now, Intelligent Commerce Connect is the infrastructure that makes autonomous shopping agents viable in mainstream consumer products within the next 12 to 18 months.

What I’d watch is which AI assistant integrates this first. The obvious candidates are products with strong shopping intent: a travel booking agent that can buy the flight, not just find it.

A grocery assistant that can reorder staples, not just suggest them.

An expense management agent that can pay vendors directly from approved budgets is another clear use case. Any product where “find it and pay for it” is the whole job stands to get meaningfully better with this infrastructure underneath it.

This also changes the best agentic AI tools in a practical way. An agent that can pay is categorically more useful than one that can’t.

Tools built on agent frameworks that support TAP, MPP, ACP, or UCP now have a clear path to adding checkout as a native feature rather than a workaround.

For merchants, the inventory discoverability layer is worth paying attention to. If AI agents become a significant shopping channel and your product catalog isn’t accessible to them, you’re invisible to that traffic. Shopify’s agentic storefront move is running the same play from the merchant side: Visa is handling the payment rail, Shopify is handling the catalog layer.

When Will AI Agent Payments Go Mainstream?

AI agent payments will reach mainstream consumer use when a major AI assistant platform ships an integrated Visa checkout flow, which is likely within 12 months given the current pilot momentum.

From what I’ve seen in how payment infrastructure moves, the pilot-to-production timeline at Visa’s scale is typically 6 to 12 months for a product with real merchant partners and established protocol support.

The four protocols Visa is supporting all have active developer communities behind them, which means agent builders won’t need to wait for Visa to define a new standard.

The bigger question is user trust, not technology. Letting an AI agent spend your money, even with spend controls, requires confidence in both the agent and the payment layer. Visa’s brand does a lot of work here.

A user who wouldn’t give an AI agent their card number directly might accept a Visa-tokenized agent credential, because the risk model is closer to a debit card with a low limit than a password in a chatbot. That framing is going to matter a lot in how this gets marketed.

Watch how AI agents for everyday users evolve over the next two quarters. The Visa infrastructure is ready.

Whoever integrates it first and makes the experience feel safe enough to use gets a significant head start in what may become one of the largest new commerce channels since mobile payments.