What Happened: OpenAI confidentially filed its S-1 IPO prospectus with the SEC on Friday May 22 2026, targeting a Q4 2026 public listing at a valuation between $852 billion and $1 trillion. Goldman Sachs and Morgan Stanley are leading the deal. The filing arrives despite OpenAI losing $1.22 for every $1 of revenue in Q1 2026.

OpenAI confidentially filed its S-1 IPO prospectus with the SEC today, Friday May 22 2026, kicking off the trillion-dollar listing every analyst on Wall Street has been forecasting for two years.

Fortune, CNBC, Reuters, Axios, and Bloomberg all confirmed the filing within hours of each other. Goldman Sachs and Morgan Stanley are leading the deal, with a public debut targeted for Q4 2026, possibly as early as September.

What nobody covering the IPO is leading with is the part that should matter most to you as a ChatGPT user. OpenAI’s S-1 has to list every material risk to investors. It does not have to list the one risk that should keep its 900 million weekly users up at night, the quiet collapse of OpenAI’s own safety promise.

In 2023 OpenAI publicly pledged 20% of its compute capacity to its superalignment safety project. According to internal reporting that resurfaced this week, the company delivered 1 to 2%. That gap, 20% promised against 1-2% delivered, sits behind everything that is about to change for ChatGPT users.

What I find striking is that almost nobody outside one Wikipedia paragraph and a single critical analysis is reporting it. So that is where I will start.

What Actually Happened

OpenAI’s IPO filing is the largest, most expensive, and least profitable tech listing of the decade.

The company filed confidentially, which means the prospectus details stay private until roughly 15 days before the public roadshow.

Goldman Sachs and Morgan Stanley are underwriting. The targeted valuation range is $852 billion to over $1 trillion, with a Q4 2026 listing window and a possible September debut.

The headline numbers from public reporting and analyst estimates are these. OpenAI is generating roughly $2 billion per month in revenue, hit an annualized $25 billion run rate by March 2026, and counts 50 million consumer subscribers plus 9 million business users. The company processes 15 billion tokens per minute through its API, with enterprise contracts now driving more than 40% of revenue.

The other side of the ledger is where Wall Street is getting nervous. OpenAI reported a negative 122% non-GAAP operating margin in Q1 2026, meaning for every dollar of revenue, the company lost an additional $1.22. That works out to a quarterly loss of roughly $6.95 billion.

For full-year 2025, OpenAI generated $13.1 billion in revenue but burned through approximately $22 billion to do it, a net loss of around $9 billion. Internal projections suggest a $14 billion operating loss for 2026.

Sam Altman’s leadership history reads like a stress test for what the SEC is about to scrutinize, and CFO Sarah Friar has reportedly pushed back internally on the timing, citing the gap between what OpenAI has promised to spend and what it currently earns.

The legal path was only cleared earlier this month when a California jury dismissed Elon Musk’s lawsuit against OpenAI, removing one of the last major institutional overhangs.

Why This Is a Bigger Deal Than It Sounds

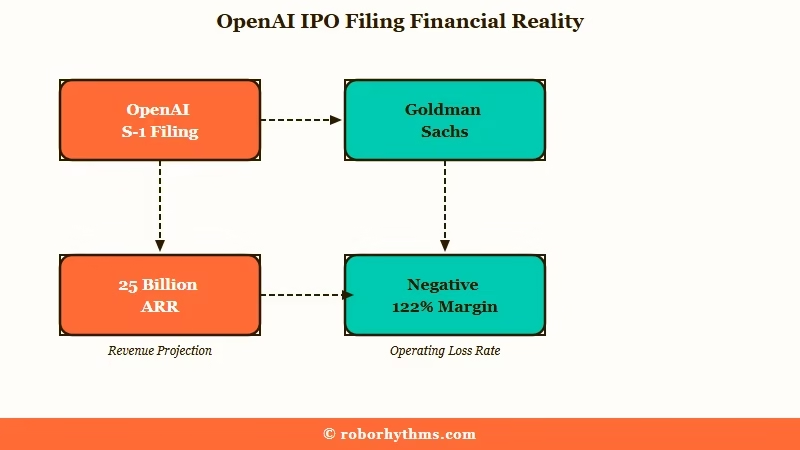

The OpenAI IPO is a forced funding event, not a victory lap. The company needs an estimated $207 billion in additional capital through 2030 just to honor its existing compute commitments, and public markets are the only pool deep enough to bridge the gap.

The way I see it, the most important number in this filing is not the trillion-dollar valuation. It is the $207 billion capital gap HSBC analysts estimate OpenAI will need to raise through 2030 to remain viable on its current trajectory. That number, sourced from an Investing.com analysis I would never have surfaced through normal news triage, explains the IPO timing better than any official statement.

OpenAI is on the hook for roughly $600 billion in compute commitments over the next five years, with some infrastructure deals stretching to $1.4 trillion over eight years. Compare that to current revenue of $25 billion annualized and the math does not close.

The IPO is not a celebration. It is a funding necessity. Public markets are the only pool of capital deep enough to bridge the gap.

The structural change that made this filing legally possible was OpenAI’s 2025 conversion from a capped-profit hybrid to a Public Benefit Corporation. Critics pointed out something the mainstream IPO coverage is glossing over.

The original investor profit cap, supposedly the moral safeguard against runaway commercial pressure, had quietly been modified years before the PBC transition to allow a 20% annual increase starting in 2025. A 20% compounding increase doubles every five years and balloons by 1000x over four decades. The cap was structurally meaningless long before the formal switch.

Microsoft’s stake is the other piece worth reading carefully. Following the restructuring, Microsoft holds a precisely 26.79% fully diluted stake valued at roughly $228 billion. The revenue share that previously had no ceiling has been capped at $38 billion total, paid out at 20% of OpenAI’s revenue through 2030 or 2032.

Microsoft is also no longer OpenAI’s exclusive cloud provider. The AGI clause that previously created legal uncertainty about when Microsoft’s rights would expire has been dropped entirely. Anthropic’s surge past OpenAI is worth holding in mind as you read what comes next.

What This Means for You

The OpenAI IPO will reshape ChatGPT pricing, the free tier, advertising, and API stability within 6 to 18 months.

Plus tier subscribers face the biggest squeeze, with internal projections showing an 80% drop. Free tier users should expect ads. API developers should expect faster model deprecation.

I would not panic, but I would prepare. Public companies have shareholders. Shareholders demand margin expansion.

Margin expansion for a company that loses $1.22 per dollar of revenue means one of two things, and probably both. Prices go up for paying users. The free tier shrinks or gets monetized through advertising.

Here is what I would expect over the next 12 to 18 months, ranked roughly by how soon you will notice each one:

- Plus tier squeeze. OpenAI’s internal projections reportedly show the $20-a-month ChatGPT Plus subscription base shrinking from 44 million in 2025 to roughly 9 million in 2026, an 80% drop, as users get pushed toward cheaper ad-supported tiers like the $5 to $8 ChatGPT Go subscription. If you depend on Plus, lock in your workflow now and have a fallback ready.

- Advertising in the chat interface. OpenAI’s internal advertising pilot reportedly hit $100 million in ARR in less than six weeks, with a $2.5 billion ad revenue target for end of 2026. Expect sponsored answers, sponsored search results in ChatGPT Search, and possibly ad slots in conversation responses. Whether that compromises the perceived neutrality of the AI is the question worth watching.

- Faster model deprecation for the API. Public companies cannot afford to keep old, cheaper inference paths alive indefinitely if newer models have better unit economics. If you build on the OpenAI API, plan for a faster sunset cycle on older models and rate-limit tightening on the lower-cost tiers.

- Feature rollout aligned to earnings calls. From what I have seen at other newly public tech companies, the release cadence shifts from “ready when ready” to “ready when the next earnings call needs a story.” Major features may get held back or rushed depending on quarterly optics.

- Agentic Commerce inside ChatGPT. OpenAI and Stripe have co-developed an Agentic Commerce Protocol that lets ChatGPT autonomously complete purchases from over one million Shopify and Etsy merchants through Instant Checkout. Once that is live and paying back commission to OpenAI, the incentive to keep you inside ChatGPT for transactions grows.

Here is the per-tier impact at a glance:

| User type | What you should expect | Timeline |

|---|---|---|

| Free tier | More ads, lower rate limits, conversion push to Plus or Go | 6 months |

| ChatGPT Plus ($20/mo) | Possible squeeze or rebranding, tier shrinks 80% in internal projections | 6-12 months |

| ChatGPT Enterprise | Most stable tier, growing 9x year-over-year, your contracts are safer | Stable |

| API developers | Faster model deprecation, rate-limit tightening on older models | 12 months |

| Casual ChatGPT user | Sponsored answers in Search, advertising in conversation | 6-12 months |

The single most concrete user-facing risk that should be in the S-1 is something the financial press is not covering. There is an active civil case, Nippon Life Insurance Company of America v. OpenAI Foundation, in which the plaintiff alleges that ChatGPT generated a completely hallucinated legal citation, Carr v. Gateway, that ended up in court filings.

That is one disclosed case. The S-1 will have to list how many similar incidents OpenAI has settled quietly or is currently fighting. If you use ChatGPT for any professional work that touches legal, medical, financial, or compliance territory, that disclosure is going to matter.

Example scenario: Imagine you currently use ChatGPT Plus to draft client emails, research industry stats, and run quick legal-adjacent checks. By Q1 2027, you might find that the Plus tier you grandfathered in has been rebranded as “ChatGPT Pro” at $30 a month with the old features intact, while a new $10 “ChatGPT Plus” tier launches with ads and reduced limits. Meanwhile your free-tier colleague sees sponsored brand mentions inside ChatGPT Search results. The neutrality you assumed was permanent turns out to have been just a pre-IPO subsidy.

What Comes Next

OpenAI’s S-1 stays sealed until roughly 15 days before the public roadshow, with a September 2026 debut as the early target. Watch for SEC feedback within 30 days, the unredacted S-1 release, the roadshow itself, and pricing day.

OpenAI’s confidential filing means the financial details stay sealed until roughly 15 days before the roadshow. The CFO has signaled internally that the company is not ready. The targeted September listing window may slip into Q1 2027 if the SEC review process surfaces accounting questions, and analysts at the Council on Foreign Relations and similar bodies have already flagged the $207 billion HSBC capital gap as a structural risk.

Here is what to watch in order. First, the SEC’s preliminary feedback on the confidential filing, which typically lands within 30 days. Second, the unredacted S-1 release, which under SEC rules must happen at least 15 days before the roadshow.

Third, the roadshow itself, where institutional investors will see financial data the rest of us only get to read after the fact. Fourth, the actual pricing day, which determines whether OpenAI lists at $852 billion (the floor) or pushes above $1 trillion.

In the meantime, the company is positioning hard. From the way I read the announcement timing, filing the same week SpaceX’s S-1 dropped is not a coincidence.

SpaceX’s prospectus disclosed Anthropic paying $1.25B monthly for compute from xAI, totaling $15 billion a year. That number put OpenAI’s own compute story in stark relief and arguably forced the timing.

If the IPO does land in September, OpenAI will close 2026 having raised roughly $200 billion across private and public capital combined. The 2027 burn rate will tell us whether that was enough.

What I would do this weekend is two things. Audit your dependence on ChatGPT for anything you cannot afford to lose access to overnight, and make sure you have at least one alternative AI assistant working in a parallel browser tab.

The IPO is happening whether you like it or not. The question is whether you are caught off guard the day Plus tier pricing changes or whether you already have a contingency in place.

How OpenAI killed automation startups is the obvious reminder that this company makes decisions on a different time horizon than the products you build on it.

Sources: Fortune, CNBC, Reuters, Bloomberg, Axios, The OpenAI Files restructuring concerns, HSBC analyst notes, SpaceX S-1 prospectus, Liberty Company Insurance Brokers (Nippon Life v. OpenAI case analysis).

Love this article. I’m a skeptic of Open AI.

But what is more powerful, the brilliant observation in your article, or the idiocy of the American Public.

Will the publics’ stupidity result in the largest IPO in history?