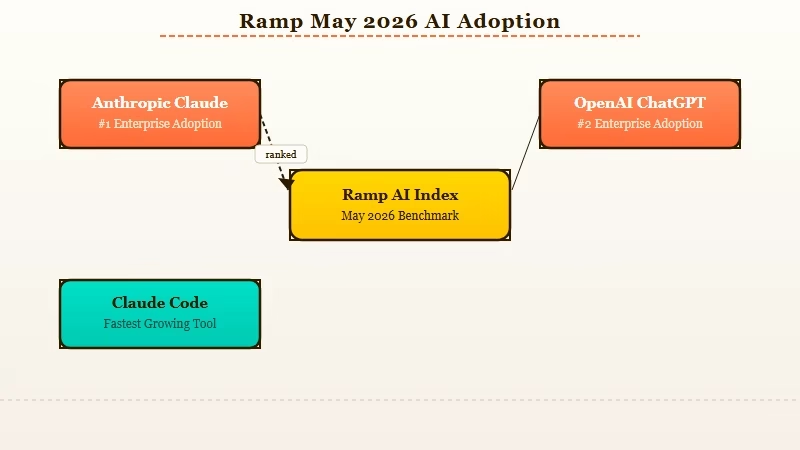

What Happened: Anthropic Claude passed OpenAI ChatGPT in US business AI spending in April 2026 with 34.4 percent adoption versus 32.3 percent, per Ramp’s May 2026 AI Index. Claude Code drove most of the gain. ChatGPT still leads on consumer use.

The Ramp AI Index dropped on May 15, 2026 with a number nobody in the OpenAI camp wanted to see. For the first time in the short history of this market, Anthropic’s Claude has overtaken ChatGPT in US business AI spending.

The story is still moving and most of the coverage so far has been written for the CFO desk, so I want to walk through what it says, why it matters, and what changes for anyone who builds or ships with these tools every day.

What I find most striking is the velocity. A year ago Anthropic was at 9 percent of the Ramp business sample. In April 2026 it crossed 34.4 percent, while OpenAI slipped from 33.3 to 32.3.

That is not the gentle drift you usually see in software procurement. Ramp’s lead economist Ara Kharazian called it “a stunning reversal in the competitive market dynamics for AI model providers” in the May report, and the supporting numbers behind that quote are even louder than the quote itself.

The Ramp dataset is built on payment data from more than 50,000 US businesses, so this is real money moving, not survey sentiment.

The flip is also one-sided: total AI adoption across the Ramp sample only hit 50.6 percent in April, which means the entire shift is happening inside the half of the market that has already picked a tool. Anyone still reading switching from ChatGPT to Claude explainers is now part of a much larger crowd.

What the Ramp May 2026 Report Found

Claude Overtakes ChatGPT in Business AI Spend is the headline takeaway from Ramp’s May 2026 AI Index, with Anthropic at 34.4 percent of US business adoption against OpenAI’s 32.3 percent in April 2026.

The Ramp AI Index tracks corporate card spending and subscription payments across more than 50,000 US businesses. The May 2026 edition, reported by TechTimes on May 15, is the first edition where Anthropic finishes above OpenAI on overall paid adoption.

The crossover happened in April. Anthropic added 26 percentage points over the prior twelve months. OpenAI lost roughly one.

From what I have seen in the underlying numbers, Claude Code is doing most of the heavy lifting. Anthropic’s terminal-native coding agent hit $2.5 billion in annualized revenue by February 2026 and roughly quadrupled its paid business subscriptions between the start of the year and mid-cycle.

A separate analysis cited in the same coverage puts Claude Code at 4 percent of all public commits on GitHub worldwide, double its share from one month earlier.

There is a parallel revenue story to go with the adoption story. As of early April 2026, Anthropic’s annualized revenue run rate sat around $30 billion, up from $9 billion at the end of 2025.

OpenAI is reported in the same window at $24 to $25 billion. The valuation conversation that ran through Anthropic surpassing OpenAI on paper earlier this spring now has a real revenue line under it.

Why This Is a Bigger Deal Than the Adoption Headline

The Claude Overtakes ChatGPT in Business AI Spend story is a bigger deal than it looks because it tracks paid coding usage by enterprise developers, not consumer chat traffic, and that workload is the one shaping every other AI product roadmap.

What I would not do is treat this as a generic “Anthropic wins, OpenAI loses” story. The Ramp numbers are paid business AI spend, weighted heavily toward developer tooling. ChatGPT still reports roughly 900 million weekly active users on the consumer side as of March 2026.

That gap will not close on the back of one Ramp report. So the right framing is sharper: the part of the AI market where companies write real checks every month has moved.

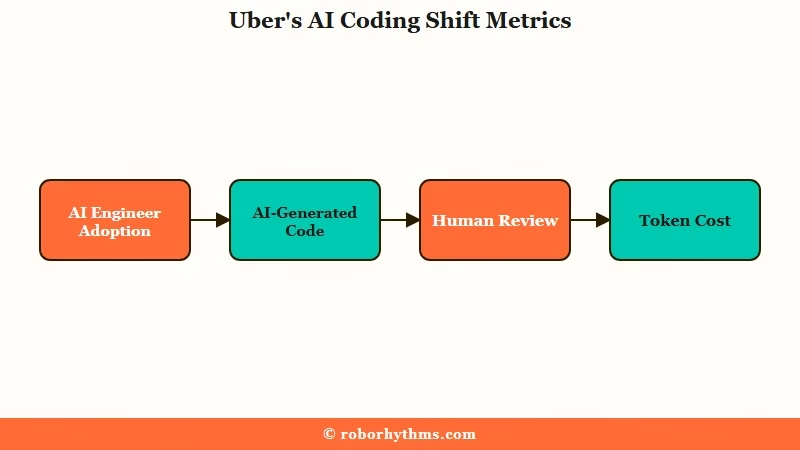

The Uber number is the cleanest illustration of why this matters. Uber CTO Praveen Neppalli Naga told reporters that AI adoption among the company’s 5,000 engineers jumped from 32 percent in December 2025 to 84 percent by March 2026.

Roughly 70 percent of committed code at Uber is now AI-generated, and 11 percent of live backend updates ship without any human review at all. Naga also gave the line I keep coming back to: “I’m back to the drawing board, because the budget I thought I would need is blown away already,” after a two-hour demo that ran $1,200 on tokens.

Here is the head-to-head snapshot on the metrics that drove the Ramp shift:

| Metric (April 2026) | Anthropic / Claude | OpenAI / ChatGPT |

|---|---|---|

| Ramp business adoption share | 34.4 percent | 32.3 percent |

| 12-month adoption change | Up 26 points (from 9 percent) | Down ~1 point |

| Annualized revenue run rate | ~$30 billion | $24 to $25 billion |

| Flagship enterprise hook | Claude Code, terminal-native agent | ChatGPT Enterprise + Custom GPTs |

| Fortune 10 customers | 8 of 10 | Reported broad coverage, no Ramp-style breakdown |

| Reliability profile | Multiple recent outages, SpaceXAI Colossus 1 deal in flight | Generally stable, scaling on existing Azure footprint |

The reason this table is interesting is that it puts the revenue gap, the adoption gap, and the reliability gap on the same page. Anthropic is winning on the first two and visibly weaker on the third, which is exactly the tension every builder is going to feel for the rest of 2026.

What This Means for You as a Builder or Solo Creator

For solo developers and creators, the Claude Overtakes ChatGPT in Business AI Spend story matters most as a workflow signal: agentic coding subscriptions and terminal-native tools are now the dominant paid AI shape, not chat-only seats.

Most of the published coverage so far has been written for the procurement and CFO audience, so the part that gets underplayed is the individual experience. From my reading of the Ramp data and the Uber commentary, here is what I would do with this news if I were running a small build today.

Before: you treated AI tooling as a single seat decision, picked one chatbot, and stayed there for a year. Token bills were small enough to ignore and the model picked itself.

After: the same decision has split. You pick a chat surface for writing, research, and one-shot prompts. You pick a separate coding agent that lives in your terminal or IDE. Token spend is now a real line item that you watch by the week, especially if you let an agent run unattended. The GPT-5.5 vs Claude Sonnet 4.6 comparison is the model-quality side of that split, but the bigger shift is the shape of the subscription.

Three practical takeaways I would put on a sticky note right now:

- Watch your token burn rate, not your seat price. The Uber $1,200-in-two-hours demo is the canary. Agent-style usage compounds fast. Set a soft daily spend cap on whichever provider you run unattended, and check it before you sleep.

- Pick a primary coding agent and a fallback. Claude Code is currently winning the paid-developer wallet, but Anthropic’s reliability is uneven enough that you want a second option you can drop in for an hour without rewriting your prompts. Local model or competitor API, either works.

- Run a refusal check on whatever you pick. Anthropic shipped a stricter safety posture, which is part of why it cleared the Pentagon dispute on principle. For creative or edge-case work that matters in your day, test the actual prompts you care about before you commit a month of spend.

If your “AI tool choice” still maps to a single chat tab, you are now behind the average paid business subscriber. That is the part the macro coverage is missing.

What Comes Next After the May 2026 Crossover

What comes next is a counter-push from OpenAI plus three real structural threats to Anthropic’s lead, all of which Ramp’s economist named on the record.

Ara Kharazian flagged the three threats by name in the May report. They are worth taking seriously because they all show up in the underlying spend data, not just in commentary:

- Per-token pricing creates a misalignment. Anthropic is incentivized to route customers to bigger, more expensive models even when smaller ones would do the job. That works in the short run and gets ugly the first time a CFO runs the math.

- Reliability is the soft underbelly. The Colossus 1 deal with SpaceXAI (220,000 Nvidia GPUs) is essentially Anthropic buying its way out of an outage problem. The SpaceX compute deal that doubled Claude limits bought breathing room, but if quality slips during the migration, the same paid developers will pivot fast.

- Cheaper alternatives are real. Open-source coding agents and lower-frontier APIs are growing off a small base. They do not need to match Claude Code on quality, only on the 60 to 70 percent of tasks where good-enough plus a price cut wins.

On the OpenAI side, the response is concrete. On May 11, OpenAI launched the OpenAI Deployment Company, a standalone unit backed by $4 billion from TPG, Goldman Sachs, and others.

They also acquired Tomoro, a London-based AI consultancy with 150 engineers. As Anthropic’s Claude for Small Business push tries to lock in the SMB workflow layer, OpenAI is doubling down on hands-on enterprise services.

As VentureBeat’s analysis put it, Fidji Simo, OpenAI’s CEO of Applications, told staff the gains were a “wake-up call” and the company must not get “distracted by side quests”.

There is also the Pentagon backdrop. In March 2026 the Department of Defense designated Anthropic a national security supply chain risk after Anthropic refused to remove safeguards against autonomous weapons.

Matt Schruers, CEO of CCIA, said the blacklisting creates “substantial business uncertainty”. For enterprise procurement teams that touch federal contracts, that uncertainty is the one number Ramp cannot capture, and it is the one most likely to swing the next index in OpenAI’s favor.

My read is that the May 2026 crossover is real and load-bearing, but the lead is fragile. The next three Ramp indexes will tell us whether Anthropic can convert a token-billed coding wallet into the broader enterprise AI category, or whether OpenAI’s consultancy-plus-deployment counter slows the bleed. Either way, the part that has already shifted is the part builders should pay attention to: paid AI in 2026 is shaped like a coding agent, not a chat tab.