What Happened: Anthropic announced a $1.5 billion joint venture on May 4, 2026 with Goldman Sachs, Blackstone, and Hellman & Friedman to push Claude into the portfolio companies of those firms. OpenAI announced a parallel, larger venture hours earlier. The “consulting industry” got hit on the same day from both sides.

The Anthropic Wall Street enterprise AI venture announced on May 4, 2026 is a $1.5 billion joint venture with three of the largest financial firms in the world, and on paper it looks like a normal funding round. It is not. It is a sales pipeline dressed up as a fund.

I have been watching the enterprise AI side of this market drift for months, and this is the move that finally clears up where the next wave of revenue really comes from. It is not from Fortune 500 marketing decks. It is from mid-sized companies that already sit inside Blackstone and Hellman & Friedman portfolios.

The same day, OpenAI announced its own $4 billion version of the exact same idea. Two of the three biggest AI labs in the world spent the same Monday telling Wall Street they want to embed engineers inside its portfolio companies. That symmetry is what makes this story bigger than the dollar figures.

What Just Happened on May 4, 2026

Anthropic launched a $1.5 billion joint venture with Goldman Sachs, Blackstone, and Hellman & Friedman on May 4, 2026, to deploy Claude inside their portfolio companies through embedded engineers.

The structure is unusual for an AI lab. Anthropic, Blackstone, and Hellman & Friedman have each committed roughly $300 million in capital, and Goldman Sachs joined as the fourth founding partner with a smaller stake. The remainder of the $1.5 billion comes from a stack of additional backers: Apollo Global Management, General Atlantic, GIC (Singapore’s sovereign wealth fund), Leonard Green, and Sequoia Capital.

The venture’s job is straightforward. It will deploy Anthropic’s Claude models inside the businesses already owned by these investors.

Engineers from the venture sit down with the operating staff at, say, a clinic owned by a Blackstone healthcare fund, and build AI tools that fit the workflows the staff already uses. That is the “forward-deployed engineer” model, popularised by Palantir, where the engineers move into the customer’s office instead of waiting at headquarters for a support ticket.

The official framing in the announcement made the model explicit. From the joint TechCrunch report on the venture: an engagement might begin with the company’s engineering team sitting down with clinicians and IT staff to build tools that fit the workflows that staff already use.

What I keep coming back to is that Anthropic is not selling Claude here. It is selling Claude plus a team of humans who will physically come and integrate it. That is a very different product, and it explains the dollar figure.

Why This Is a Bigger Deal Than the Headlines

The venture is structured to hand Anthropic preferred sales access to thousands of mid-sized businesses that the founding investors already own, which is the most concentrated enterprise AI distribution channel ever built in this industry.

Wall Street firms own a staggering number of mid-market companies. Blackstone alone has more than 230 portfolio companies across private equity, real estate, and credit, and Hellman & Friedman owns dozens more.

Goldman Sachs has direct relationships with thousands of mid-market clients across its asset management and investment banking arms. Add Apollo, Sequoia, and General Atlantic to the list and the addressable customer set is in the tens of thousands of operating businesses.

The way I see it, the venture is less about $1.5 billion in capital and more about a pre-built customer list. Most enterprise AI deals fail at the procurement stage, not the technical stage, and the buyer cycle is six to eighteen months.

With this venture, Anthropic skips that. The owner of the company is also the investor in the AI venture, and procurement becomes a phone call between two partners at the same firm.

There is a useful comparison here. Looking at the Anthropic Mythos review, the consumer side of Anthropic has been moving slowly through a crowded retail market.

The enterprise side has not had a clear moat. This venture is the moat, and it locks Claude into a portfolio of buyers that competitors would need years and hundreds of sales reps to even reach.

The OpenAI parallel matters too. OpenAI’s own venture, called The Development Company, is targeting $4 billion at a $10 billion valuation, with 19 investors including TPG, Brookfield Asset Management, Advent, and Bain Capital. There is no investor overlap between the two ventures.

The Wall Street AI services market has been carved into two non-overlapping spheres of influence, on a single Monday, by the two biggest model labs in the world. That kind of clean partition does not happen by accident.

What This Means for AI Tool Buyers and Builders

If you sell AI tools to mid-market companies, this venture just changed the rules of who you are competing against and how distribution really works.

Three things shift starting this week, the way I see them:

- Distribution stops being neutral. Until now, a better AI product could win on a normal evaluation, but going forward the customer’s owner has a financial interest in deploying Claude or GPT specifically. A third-party tool now has to fight not just on features but against the fund’s own profit motive.

- Forward-deployed engineering becomes table stakes. Palantir already proved this works. Anthropic and OpenAI just confirmed it. If a tool wants to land a multi-million-dollar enterprise contract in 2026, it needs human integration support, not a docs site. SaaS companies that ship pure software and call it a day will be locked out.

- The mid-market is suddenly the prize. Most AI commentary fixates on Global 500 buyers. The actual money in this venture is targeting mid-sized companies. That is where headcount is high, IT teams are small, and a forward-deployed engineer can replace three contractors. Anyone building for the long tail just got a clear signal that the long tail is where the next $10 billion comes from.

For comparison, the Microsoft Agent 365 review covers a similar move from Microsoft into the enterprise governance layer. The difference is that Microsoft is selling a platform, while Anthropic is now selling consulting. Two different bets on what the real bottleneck is.

The Forward-Deployed Engineer Bet, In One Table

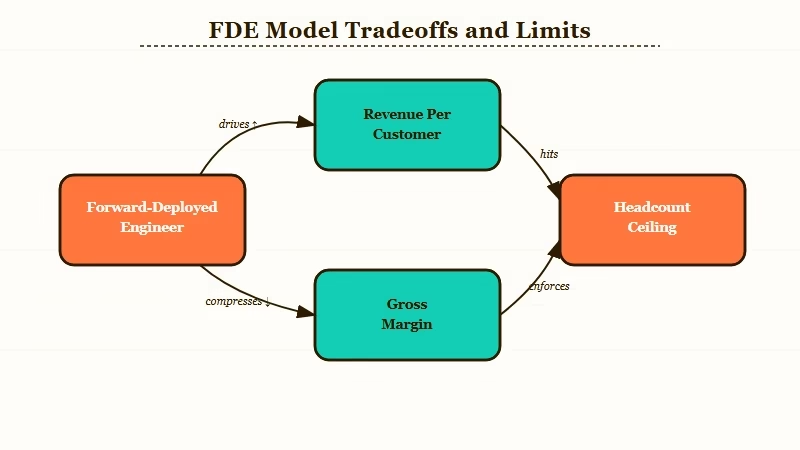

The forward-deployed engineer model is what makes this venture work as a sales channel and what limits it as a scalable business, all at the same time.

The way I see it, the FDE model is the load-bearing decision in this venture. It is also where the venture is most likely to break. Here is what the math looks like for a single engagement.

| Engagement variable | Typical SaaS deal | Forward-deployed engagement |

|---|---|---|

| Sales cycle | 6 to 18 months | 4 to 8 weeks (warm intro from owner) |

| Engineers per customer | 0 (self-serve) | 2 to 5 dedicated |

| Annual revenue per customer | $50k to $500k | $1M to $10M |

| Margin profile | 70% gross | 30 to 45% gross |

| Scaling constraint | Server cost | Engineer headcount |

The trade-off is obvious. Higher revenue per customer, much lower margin, and a hard ceiling on how fast the venture can grow.

Here is how I would frame the difference for any builder who is thinking about whether to ship pure SaaS or move toward the FDE model in 2026:

Before: “We will sell our AI tool through a self-serve product-led growth motion. Sign-ups go up, costs stay flat, the platform scales.”

After: “We will sell our AI tool to one mid-market customer at a time, embed two engineers for eight weeks, charge $1.5M per engagement, and raise prices once the workflow is integrated. We will not scale past 200 customers without acquisitions.”

Anthropic cannot 10x this venture without 10x-ing its engineering payroll, which is the exact constraint that turned Palantir into a niche-but-profitable company instead of an Oracle-scale one.

What Comes Next, By My Read

The next 90 days will produce a wave of mid-market AI consultancy acquisitions, a counter-move from Google, and a slow-bleed squeeze on boutique consulting firms.

The most underdiscussed part of this announcement is what happens to mid-market AI startups in the next 90 days. From what I can see, three patterns will play out.

First, expect a wave of acquisitions. The fastest way for the Anthropic venture to scale headcount is to buy small AI consultancies that already have the engineers.

Watch for $10 to $50 million tuck-in deals in vertical-specific consultancies (healthcare AI, legal AI, ops AI). The capital is now sitting in the venture and can be deployed directly.

Second, OpenAI’s bigger venture will probably draft a counter-move from Google. DeepMind and Google Cloud have a deeper distribution channel than either Anthropic or OpenAI, but it has been split across product teams. A vertical enterprise AI services venture from Google would be the obvious response, and the fact that Google has not announced one yet is itself a signal worth tracking.

Third, the consulting industry hit Fortune flagged is real, but it is a slow bleed, not a sudden death. Accenture, Deloitte, and McKinsey will still control the largest enterprise AI deals through 2027 because their existing client relationships are stickier than Anthropic’s investor list. The bleed shows up at the mid-market layer first, where boutique consultancies will get squeezed between FDE-equipped AI labs and the big four.

For any reader thinking about this from the builder side, Anthropic’s $30 billion revenue trajectory is the right context. That number assumed pure-play enterprise SaaS revenue, and this venture changes the mix toward services, which means slower growth but stickier accounts.

The valuation question that follows is whether $900 billion is too high for a services business or still too low for an AI-services hybrid that owns its distribution. I lean toward the latter, but it is the question every buyer of Anthropic’s reported $50 billion fundraise should be asking right now.

The thing that surprised me most in the reporting is how clean the investor split is. With $1.5 billion on one side and $4 billion on the other, and zero overlap between 22 separate firms, somebody at the boardroom level had to coordinate this.

That kind of pre-arranged segmentation is what mature industries do, not what hyper-competitive infant industries do. The enterprise AI services market just declared itself a mature industry, on May 4, 2026, before most of its customers even knew the market existed.