My Take: The AI bubble crash everyone is waiting for has already started, just not where people are looking. The application layer is dying. The foundation layer has the strongest balance sheets in tech history. Watching the wrong number is how you miss the real story.

The AI bubble crash warning has been the same Reddit post for two years now.

This week’s version came from u/reasonablejim2000 on r/artificial, ran a spreadsheet through GPT for $10 in compute (10x subsidised, $100 actual), and concluded the whole thing is going to “crash and crash HARD”. The thread sits at 759 upvotes. The top reply, at 549 upvotes, is one sentence: “who is scamming you and can I join in?”

The way I see it, that ratio tells the story. The bubble-crash narrative gets attention. The technical pushback gets the votes.

The thing nobody on either side of the thread says out loud is that the crash they are arguing about is already happening, just not at the layer they are watching.

MIT Labs published it cleanly in April 2026: 95% of organisations are getting zero return on their AI pilots. PwC’s same-month study said 74% of AI’s economic value is being captured by just 20% of organisations.

Those are not bubble-warning numbers. Those are mid-crash numbers.

This piece argues that the AI bubble crash people are waiting for at the foundation layer is not coming, that the crash at the application layer has already arrived without a headline, and that confusing the two is how investors and operators both end up holding the wrong end of the trade.

According to Goldman Sachs Research’s bubble analysis, AI capex at 0.8% of GDP is barely half of the 1.5% threshold reached during prior tech booms, and the leading companies are sitting on the strongest balance sheets the sector has ever had.

The Mainstream View and Why It Falls Short

The mainstream AI bubble crash view says foundation-model providers are burning unsustainable capital and a 2026 stock correction is imminent.

It is the wrong frame and the wrong layer.

Iram Ahmed laid the case out in his AI reckoning piece earlier this year. Pieces from FXEmpire, articsledge, and a steady drumbeat of Substack writers have said the same thing.

The argument runs: AI infrastructure spending hit $400 billion in 2025 against only $100 billion in enterprise revenue, circular financing between Nvidia and OpenAI and Microsoft and Oracle inflates the numbers, valuations are bubble-shaped, and a credit-tightening 2026 ends it all in a Cisco-2000-style crash.

What this view gets right: the gap between infrastructure spend and enterprise revenue is real, the circular financing pattern is real, and the application-layer use cases are mostly garbage. I would not argue any of those points.

What this view gets wrong is the conclusion that the crash happens at the stock-price level for Nvidia or OpenAI. The leading AI companies have balance sheets that make late-1990s telecom or Pets.com look like a lemonade stand.

The capex ratio to GDP is half the 1.5% threshold that historical booms reached before collapsing. The Jevons effect (lower per-token costs multiply total demand rather than reducing it) is still running.

The crash the mainstream view is waiting for would require a sudden revenue collapse at the foundation layer. From my reading of the actual Q1 2026 numbers, the foundation layer revenue is growing 9x to 900x year over year depending on the segment. That is not a curve that crashes from above.

What’s Actually Happening at the Application Layer

What’s actually happening is that the 95-percent pilot failure rate is the crash, and it is already at full intensity.

The MIT Labs report on Q1 2026 enterprise AI pilots is the most underread document of the year.

The way I read the MIT and PwC numbers is straightforward. Companies are still announcing pilots; pilots are still failing; failed pilots quietly do not get renewed.

The headline keeps reading “AI investment grows 75 percent” while the underlying reality is “the same 20 percent of organisations capture 74 percent of the value, and the other 80 percent are slowly bleeding budget on things that do not work”.

From my view of how this maps to specific business categories:

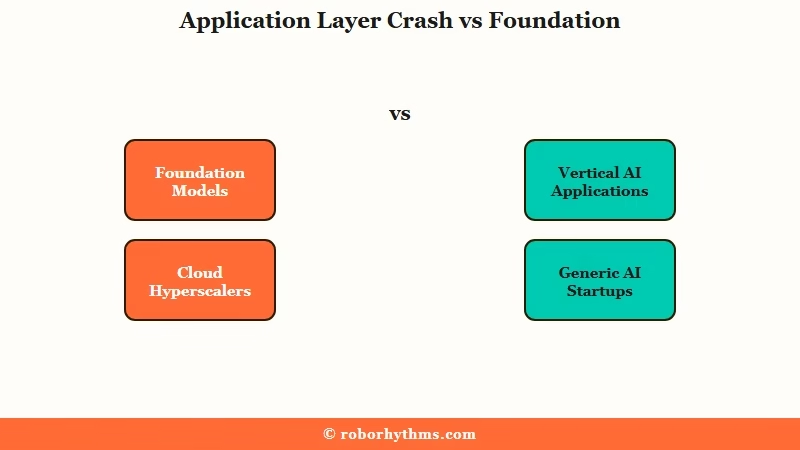

| Layer | What’s happening | Crash status |

|---|---|---|

| Foundation models (Anthropic, OpenAI, Google, xAI) | Revenue growth outpacing capex curve | Not crashing |

| Cloud hyperscalers (Microsoft, AWS, Google) | AI revenue mix shifting up double digits | Not crashing |

| Vertical AI applications (most SaaS GPT wrappers) | 95% zero-return pilots, ARR not renewing | Already crashed |

| Generic “AI assistant” startups | Funding rounds collapsing in late-stage extension | Crashing now |

| AI infrastructure (Nvidia, networking, energy) | Order book firm through 2027 | Not crashing |

What I would call out specifically is that the “AI startup” category death is happening on a roughly six-month lag from when the application launches.

A company that raised a Series A in October 2025 on a “we wrap GPT-5 to do X” pitch is now hitting renewal cycles where the customer realises they could just call the API directly for a quarter of the price.

That is the crash. It is not televised because nobody owns shares of those companies.

For the broader argument on why agent-shaped AI applications fail in production environments, why AI agent demos fail covers the specific failure modes that drive the pilot mortality rate.

The Part Nobody Wants to Admit

The part nobody wants to admit is that most of the AI companies dying right now deserve to die, and the foundation-layer concentration is the natural shape of the industry, not a bubble.

The bubble framing makes everyone a victim. The reality is that most application-layer AI was a thin wrapper on someone else’s API and was always going to be commoditised.

From what I have seen across the application landscape, the “AI startup” graveyard of 2026 is full of companies that did one of three things: built a GPT wrapper with no proprietary data moat, sold a vertical AI tool that the foundation model could absorb as a feature, or pitched “AI-powered” without ever specifying what the AI was doing differently from a regex and a templated response.

The same dynamic ran during the 1999 dot-com era, and the parallel that nobody draws is the one that matters. The 2000 crash killed pets.com and webvan and a thousand other companies that mostly should not have existed. It also did not kill Amazon, Google, or the underlying internet infrastructure.

Amazon’s stock dropped 90 percent and then came back over the next decade because the business model was real. Pets.com did not come back because the business model was not.

What I would argue is happening in 2026 is the exact same sorting function. Foundation-layer companies (Anthropic, OpenAI, Google, Microsoft) have business models that work even at unsubsidised pricing.

Wrapper-layer companies do not. The market is figuring out which is which.

The unwelcome implication is that the venture capitalists and operators who built application-layer AI startups in 2024 and 2025 were not investing in “AI”; they were investing in regulatory arbitrage on subsidised compute. The arbitrage is closing. The startups are dying.

That is correct, healthy, and being misread as a sector-wide crash.

The way I would reframe a typical “AI bubble” pitch in your head:

Before: “AI infrastructure spending hit $400 billion against $100 billion of revenue. That gap is the bubble. Crash incoming.”

After: “AI infrastructure spending hit $400 billion against $100 billion of revenue. The $300 billion gap is mostly enterprise pilot spend that will not renew, not foundation-layer overbuild. The crash is at the pilot layer, has been running for two quarters, and is the system working as designed. The foundation-layer balance sheets are fine.”

For a related read on why so many enterprise AI agent projects collapse before they hit production, why AI agents keep failing covers the operator-level failure pattern that drives the pilot-mortality numbers.

What to Watch Instead of the Bubble Crash Headlines

What to watch instead is the pace of foundation-layer revenue growth and the rate at which application-layer companies are renewing customer contracts.

Those two numbers tell the actual story. The Nvidia stock chart does not.

The way I would track this if I were running an AI investment thesis or a content-business decision:

- Watch foundation-model revenue growth on a six-month basis. If Anthropic, OpenAI, Google, and Microsoft are all still posting double-digit quarter-over-quarter growth at the end of 2026, the foundation layer is not crashing.

- Watch the share of compute capacity that runs at actual unsubsidised pricing versus the share that runs at promotional or enterprise-pilot pricing. The latter is the bubble. The former is the business.

- Watch the application-layer renewal rate at 12 and 18 months. If “AI startup” customers are renewing at the rate normal SaaS customers do, the application layer is healthier than the pilot numbers suggest. If renewal rates are collapsing, the application crash is still mid-flight.

- Watch the Mac Mini and Mac Studio supply chain for consumer compute capacity, since the Mac Studio shortage is the most underrated signal that local-LLM demand is rising rapidly and may eat into the cloud-pricing assumption that the entire foundation-layer revenue forecast rests on.

- Watch the pattern of AI startup acquihires versus shutdowns. Acquihires mean the foundation-layer players are extracting value from failed wrappers. Shutdowns without acquihires mean the value was never there.

What I would do in practice is read those five signals quarterly and ignore every “bubble bursting” headline that does not explicitly cite at least three of them. The headlines are a sentiment market. The numbers are the actual market.

Hot Take

The AI bubble crash narrative is a coping mechanism for people who missed the trade and want it to be coming. The actual crash is already running at full speed, has been for at least two quarters, and is killing exactly the right companies.

Anyone selling you a 2026 “imminent burst” thesis without naming MIT’s 95% pilot failure number, PwC’s 74-20 value concentration, and the foundation-layer balance sheets is selling you a vibe, not analysis.