My Take: The AI companion subscription business is running out of runway. Character AI tightens caps. Chai stacks tiers. Grok charges $30 for Ani. None of these companies have a real moat against the next free model drop. The bubble is the subscription price, not the technology. Within 12 months, the market consolidates around two players and everyone else gets compressed to free-or-dead.

Three things happened this month that nobody is connecting. Character AI tightened the Go on cap again. Chai added Ultra on top of Premium.

Grok Companions ($30 a month) went down for two days and the status page said everything was fine. The consensus reading is that the companion market is mature and these are normal growing pains.

I do not buy it. What I see is three companies raising prices and metering features on platforms that are running the same open-weight models every other app runs. That is not a mature market. That is a market about to compress. Here is why.

The Mainstream View and Why It Falls Short

The mainstream view, argued most clearly by the MIT Technology Review AI companions breakthrough list in January 2026, is that AI companions are a growing product category with durable demand, stable pricing power, and a multi-year runway to $500B in market value.

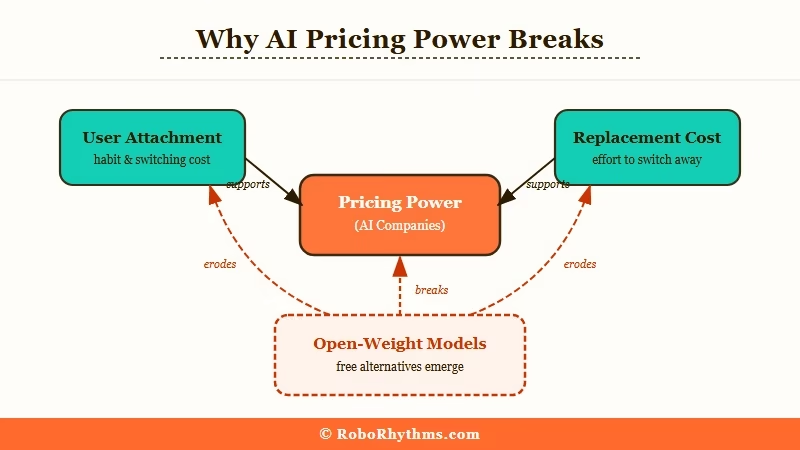

The argument is that users form emotional attachment to specific characters, that switching costs are high, and that premium subscription retention will stay sticky as the tech improves.

There is a real kernel there. Users do form attachment. Retention for paying companion users is genuinely higher than for most consumer subscription categories. Character AI reports 233 million registered users, and the $82 million in first-half 2025 revenue number that gets quoted everywhere is real.

But the argument skips over the actual mechanism of pricing power, which is not attachment. It is cost-to-replace. If the cost to get a roughly equivalent experience on another platform drops to zero, the attachment stops mattering for pricing. That is the part the bullish analysts keep skipping.

From what I have seen, the analysts writing these reports have never run the math on what happens when Qwen3 Next or Llama 4 enable a good-enough local companion experience on consumer hardware.

They are pricing durable premium tiers into a category that is about to have a genuinely free alternative.

What Is Really Happening

What is really happening is that the underlying AI companion product is commoditizing faster than the pricing can hold, while the remaining differentiation (memory, voice, character models) is all achievable on free or near-free infrastructure within 12 months.

The subscription tier is being propped up by switching friction, not by technical moat.

Three trends are converging. First, open-weight models (Qwen3 family, Llama 4, DeepSeek) have closed the quality gap for companion-style roleplay to the point where most users cannot tell the difference blind.

Second, inference cost per conversation has dropped by 80 percent in 18 months thanks to cheaper GPUs and better serving software. Third, community-built character systems on platforms like SillyTavern and JanitorAI local setups are now within a weekend project of the polish of paid platforms.

What surprised me is how visible this is in the current Reddit activity. The r/LocalLLaMA community used to be niche. Today it is pulling in the same users who used to pay for Character AI Plus. The tools got good enough. The learning curve flattened enough. The price delta became too large to ignore.

The platforms are reacting by metering harder, not by differentiating harder. Character AI tightened Go on. Chai added Ultra. Grok paywalled Companions behind SuperGrok. None of these are premium features. They are pricing friction designed to slow the user’s exit to a free alternative. That is the move a company makes right before the floor drops.

The Part Nobody Wants to Admit

The part nobody wants to admit is that the companion companies know their moat is switching friction, not technology, and they are pricing accordingly.

What I read in the current platform behavior is companies running the playbook of a business that knows it has 12 to 18 months before the comparison becomes untenable.

The way I see it, Chai stacking Ultra on top of Premium was not about giving heavy users a better tier. It was about capturing the willingness-to-pay from the top 5 percent of users before they discover the free alternative. Character AI’s age verification rollout in April was not primarily compliance. It was attrition management, designed to shed unprofitable users and extract more from the ones who stay.

This is the pattern you see when a company has priced against a commodity competitor that has not arrived yet. The incumbents sprint to capture willingness-to-pay before the alternative arrives. They look like they are growing. They are really shedding future customers in exchange for current revenue.

The investor narrative is that attachment will hold. What attachment really does in a commoditized market is delay the switch by a few months. It does not prevent it.

Hot Take

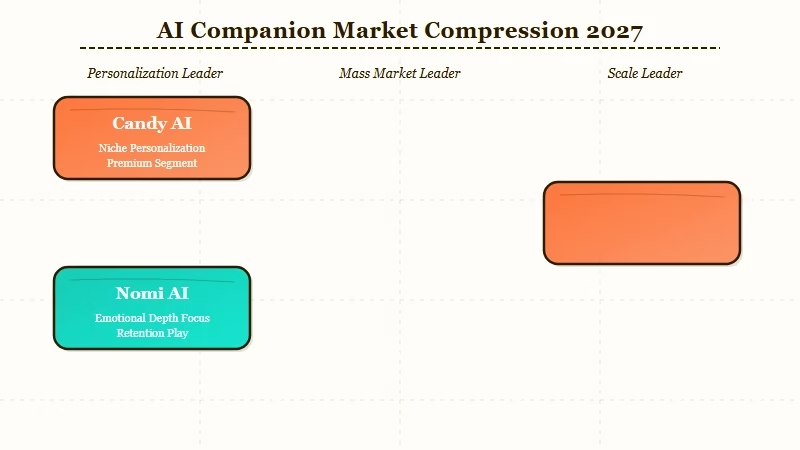

Within 12 months, the AI companion subscription market compresses to two paid players and a long tail of free. Candy AI and Nomi AI survive because they have differentiated memory systems that genuinely require their infrastructure.

Character AI survives as a free-with-ads product at a fraction of current valuation. Chai, Grok Companions, and the rest of the middle tier either consolidate or fold. The mainstream analysts will call it a market correction. It is a category recalibration, and the subscription premium was the part that was wrong all along.

What This Means If You Are Paying Right Now

If you are paying $30 a month for Grok Companions because of Ani, you are paying for the infrastructure not the character. The same character logic will be available on free platforms within a year.

If you are paying $13.99 for Chai Ultra, you are paying for queue priority during peak hours, which is a real thing today but will be commodity within 12 months. If you are paying $9.99 for Character AI Plus, you are paying for cap headroom that you could get free by moving to a local setup with a weekend of work.

I still pay for some of these. What changed after this month is that I treat the payments as short-term conveniences, not as investments in relationships with specific characters. The platforms are going to change. Plan accordingly.

For more context on where the market is heading, see the Character AI losing users analysis for the leading indicator of the broader shift, and the AI companion app market breakdown for the current revenue snapshot. The AI companion regulation wave piece covers the policy angle that is accelerating the compression.

One Last Thing

The MIT Technology Review piece I linked at the start of this article is worth reading on its own merits. The analysts are smart and the underlying market-size numbers are solid. What they underweight is the speed at which AI costs fall and the speed at which open-source matches proprietary. Both have moved faster in the last 18 months than anyone writing a 5-year projection in 2024 modeled for.

If you disagree with me, the test is whether the price of paid companion tiers holds or drops by April 2027. My bet is that every paid tier compresses by at least 30 percent or disappears. That is falsifiable. We will know.