My Take: Kleiner Perkins raising $3.5B is being reported everywhere as proof that AI investment is healthy and the opportunity is wide open. The real story is different. When growth-stage money starts flowing at this scale, it means consolidation has begun. The window where small builders could compete against institutional capital just got noticeably smaller.

The Mainstream View and Why It Falls Short

The mainstream view is that Kleiner Perkins’ $3.5B raise proves AI is a durable investment category, not a speculative bubble running out of steam.

TechCrunch’s headline framed it as going “all in on AI,” and coverage across the rest of the tech press tracked in the same direction. A 50-year-old firm nearly doubling its previous fund size in less than two years reads, on the surface, like an institutional endorsement of the entire category.

I get the appeal of this reading. If the sophisticated money is pouring in, the technology must be maturing. The fear that AI is a speculative sugar rush starts to look paranoid.

Why This Reading Is Wrong

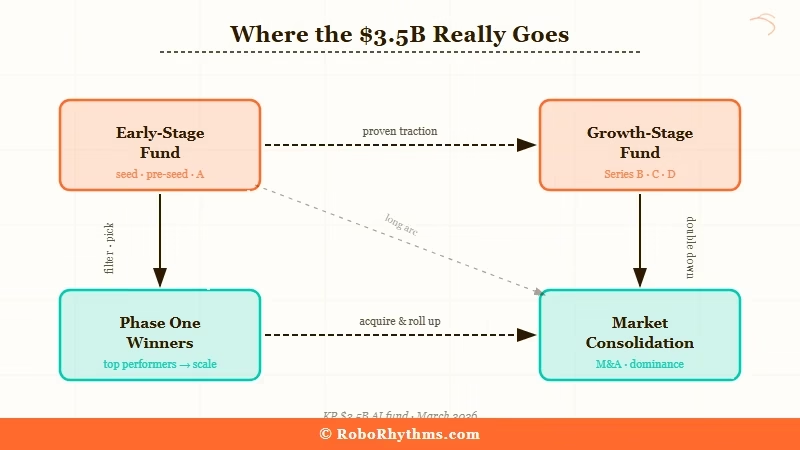

The problem is the structure of the raise. $1B of the $3.5B goes to KP’s 22nd early-stage fund. The other $2.5B targets growth-stage companies.

That split is almost never discussed in the coverage, and it changes the meaning of the headline entirely.

Growth-stage capital does not fund new ideas. It funds companies that already have product-market fit, paying customers, and a defensible position.

That $2.5B is not expanding the opportunity for builders. It is concentrating it into the hands of whoever already won round one.

What Is Really Happening

What is really happening is a structural shift from a fragmented AI market with hundreds of viable entry points to a capital-concentrated one where a small number of well-funded companies will absorb most of the value.

The way I see it, there were two distinct phases. Phase one (2023 to 2024) was defined by API access as the moat. If you could integrate faster than anyone else and build a product people would pay for, you could compete.

That window was narrow but real. Phase two started sometime in 2025. The companies that won phase one started raising institutional rounds.

They now have retention data, brand recognition, and small business AI tools embedded into workflows that are genuinely hard to displace. KP’s $2.5B growth-stage capital goes to those companies, not to the next person building something new with a credit card and an API key.

| Signal | 2024 | 2026 |

|---|---|---|

| Who wins with API access | Anyone who ships fast | Companies with data moats |

| VC focus | Early-stage seed funding | Growth-stage scaling rounds |

| Competitive moat | Model quality and speed | Proprietary data and distribution |

| Infrastructure costs | Stable or declining | Rising (memory chip shortage) |

| Entry barrier for new builders | Low | Rising sharply |

The Infrastructure Problem Behind the Headlines

What I find particularly troubling is that capital concentration is accelerating while the underlying infrastructure is getting more expensive, not less.

Data centers now consume roughly 70% of all memory chips produced globally in 2026, a share that Tom’s Hardware projects will keep supply constrained through at least 2028.

API costs feel stable right now because large providers are absorbing the squeeze. That situation has a limit.

The large companies have signed long-term supply contracts with memory manufacturers. The independent builders have not.

The Part Nobody Wants to Admit

The part nobody wants to admit is that “just use the API and build something” stopped being a viable competitive strategy sometime in the last twelve months, and most independent builders have not fully absorbed that.

From what I’ve seen, the builders who are winning in 2026 are not winning because they have better model access than their competitors. They are winning because they built proprietary data loops, retention mechanics, or distribution advantages during the phase-one window.

The model has become a commodity. The data pipeline and the distribution channel have not.

This mirrors exactly what OpenAI did to automation startups when it started building native features for things that independent builders had been charging for as standalone products. When institutional capital backs the incumbents at scale, it accelerates the same pattern across every AI category simultaneously.

The uncomfortable implication is direct: if you are an independent AI builder without a data or distribution advantage today, the KP raise is not good news. It is a signal that the clock is ticking louder. The question is what you do with that signal.

What Independent Builders Should Do Right Now

The time to act on this is before the growth-stage money fully deploys and every category gets locked up. From my experience watching how AI markets have shifted over the past two years, four moves matter most:

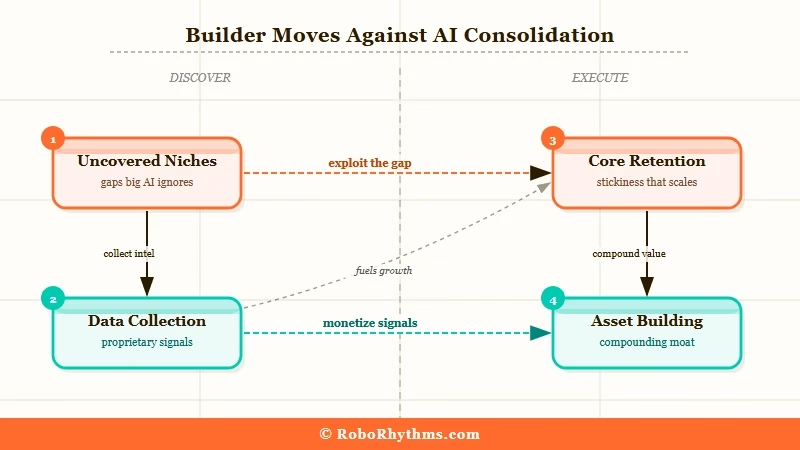

- Pick a category where growth-stage incumbents have not yet raised institutional rounds. Niche verticals, specific professional workflows, and high-trust companion experiences that large platforms avoid are still wide open.

- Prioritize data collection over feature shipping. Models will keep improving regardless of what you do. Your proprietary data will not magically appear if you wait.

- Build retention mechanics into the product’s core, not as an afterthought. Retention is the one moat that growth-stage capital cannot simply buy away from a competitor.

- Study what AI automation agencies are getting wrong and do the structural opposite. Most are trading time for money. The builders who survive consolidation are building assets.

Hot Take

Every VC raise in AI gets reported as proof the ecosystem is open and healthy. The implication is that independent builders should feel encouraged. I think the logic runs the other way.

Every growth-stage raise signals that a category got locked up. When Kleiner Perkins puts $2.5B behind companies that already won, they are not funding the future of AI. They are cementing who controls the present.

The builders who will matter in two years are the ones who read that raise as a starting gun, not as validation that things are going well.

Quick Takeaways

- Kleiner Perkins raised $3.5B, but $2.5B of it targets growth-stage companies that already won phase one

- Growth-stage investment signals consolidation, not an expanding opportunity for independent builders

- The infrastructure pressure is real: data centers consume 70% of global memory chips with no relief until 2028

- The competitive moat in AI has shifted from model access to proprietary data and distribution

- Independent builders should treat each institutional raise as a deadline, not a confidence signal